![]()

NOTICE OF EXTRAORDINARY GENERAL MEETING

This communication is to advise members of Heaton Stannington Football Club of an EGM (Extraordinary General Meeting) which will be held at Grounsell Park on Monday 11 July 2022, 19:00. The purpose of the meeting is to set out details of a restructuring of the Club and seek agreement to proceed with the proposals. This communication sets out details ahead of the meeting.

Introduction

The purpose of this communication is to inform members, in as simple a way as possible, given the issues set out below, how we as a committee have had to take action to consider viable options for the proposed restructuring of the Club in order to remain compliant with applicable regulations arising from our CASC status. As part of that process, we have taken extensive legal and accounting advice on what it will mean for you as members before arriving at this decision. Please be assured that you’ll still be a member of Heaton Stannington and enjoy all the benefits your current membership brings with it. However, it is a recommended and indeed necessary solution to ensure that we can continue as a CASC and meet the requirements set out by HMRC.

Background

The Club is an unincorporated association members’ club, which amongst other things means that the Committee is ultimately responsible for acts undertaken and liabilities arising in its name. In 2005 the Club applied for and was registered as a Community Amateur Sports Club (CASC). This ensured the Club could enjoy certain tax benefits, but it required the Club to adopt certain characteristics, to fulfil certain conditions and to remain compliant with them. In 2015, new regulations were then introduced to tighten up CASC operating and trading activities. In summary, as a CASC, we must:

- Remain within certain financial thresholds for trading purposes, both with our members and third party guests (including away teams and their supporters), for VAT and Corporation tax purposes

- Not pay players in excess of £10,000 per year in aggregate (excluding expenses for away games and tours), and

- Ensure at least 50% of the membership must take an active part in the sport.

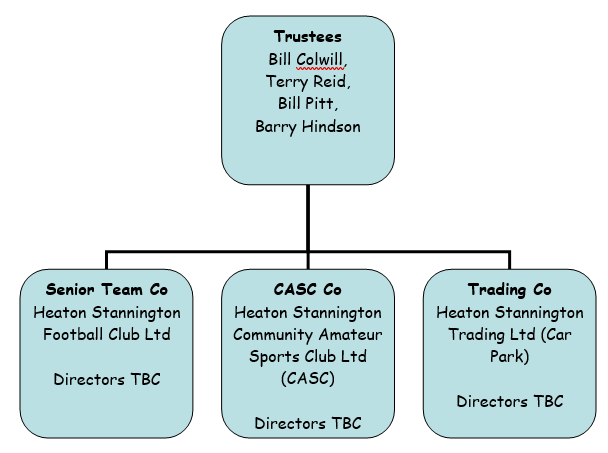

Where a CASC feels that it can no longer remain within the regulations it must either de-register or take appropriate action to ensure that it can remain compliant. De-registration would not be viable for the Club since it could face a potential Capital Gains Tax liability which could effectively close the Club. HMRC actively encourage organisations to take action where appropriate in order to ensure compliance. You may recall we took action to incorporate Heaton Stannington AFC Car Parks Limited, in order to separate this trading income from participation-based income in line with the CASC regulations. This also brought a number of tax benefits, which will continue in the proposed new structure. Action is necessary now, brought about by the success on and off the pitch in terms of turnover which has increased dramatically over the last two years. Current Structure Heaton Stannington AFC (the CASC) has four Trustees whose role it is to set the direction and strategy for the club going forward. They also hold the legal interest in the land and provide a check and balance on the Committee taking decisions which may be to the detriment of the Club and its members. The day-to-day management of the Club and all its entities and assets are delegated to the Committee. Heaton Stannington AFC Car Parks Limited has seven Directors from a mixture of Trustees and Committee members and is wholly-owned by the CASC. New structure The existing Trustees will remain as they are as custodians of the Club’s land. The Club will then form two new companies limited by guarantee, in addition to Heaton Stannington AFC Car Parks Limited.

- The first guarantee company will register as a CASC and acquire such part of the Club’s assets and undertaking as relate to community participation activity (CASC Co).

- The second will operate the senior men’s representative first team (Senior Team Co), since it is elite in nature.

The trading activities Heaton Stannington AFC Car Parks Limited (Trading Co) will expand to include all commercial trading activity, including car park, bar and catering (other than match days). Ownership of Trading Co will pass from the Club (acting by its Committee) to CASC Co, so it will in effect remain a wholly-owned subsidiary with the CASC Co as the shareholder, and therefore able to Gift Aid its profits tax efficiently by annual donation back to the CASC.. Directors will be elected for each company and there may be some (but not all) common directors of each company. Senior Team Co will be expected to meet its operating costs and, if possible, donate any profit back to the CASC. The social club will be comprised within the CASC Co and Trading Co group, subject to membership numbers, bearing in mind we have to ensure that at least 50% of the membership must take an active part in the sport. CASC Co will operate the reserve team and any future junior set up. So, this will give us the following structure: Note the actual names of each company have yet to be finalised

Benefits

- Maintains our CASC Status and the tax benefits and efficiencies which we enjoy currently as a result

- Clear separation of activities to ensure compliance with applicable regulations

- Increased revenue to fund improvements

- Any surpluses made by Senior Team Co and Trading Co will be gift aided back to the CASC, providing revenue for future development plans and improvements.

Conclusion

Having taken extensive accounting and legal advice, we consider this action has to be taken to protect our CASC status and the benefits which arise from that. Failure to take any action could lead to not having a club going forward. We intend to hold an Extraordinary General Meeting on 11TH July at which our legal advisor and current committee will be on hand to offer further explanation and answer any questions you may have. Resolutions to be proposed at the meeting shall be displayed on the Club notice board not less than 10 days prior to the EGM in accordance with Rule 10.

The Heaton Stannington Committee